다른 재벌회장들과는 다른 느낌이었고, 호탕하고 남자답고 그런 삶을 사는 사람이구나 싶었다. 언젠가 동아그룹이 파산했다는 소식도 안타깝고, 우리 삼촌도 리비아 대수로 공사에 참가했었기에 동아그룹의 파산은 내게도 아주 의미없는 그런 일은 아니었다. 당시 수많은 회사들이 무너져가던 시기라 놀라운 일은 아니었지만, 후에 나이가 들고 세상을 좀 안뒤에 알게 된 것은... 그들이 경영을 잘못했다는 이유만이 아니었다는 것이다. 사람(?)에게 잘못보인 탓에 바람앞에 촛불처럼 사라진 회사들도 있다는 것이 정말 어이가 없었다.

아무튼, 이 분이 모아나운서와 살림을 차렸느니 하는건 내겐 뉴스가 되지 못했었다. 나는 그가 기업파산이후 어떤 돈이 있었는지는 모르겠으나, 동아방송기술대학이라는 곳을 설립했다는 소식을 들었을때 다시 관심이 갔었다. 아마 그 아나운서의 영향도 있었으리라 짐작해본다. 그 동아방송기술대학의 방송차량이 우리 교회 새벽예배를 중계하기 위해 교회앞에 서 있을때마다 난 최원석 회장의 얼굴을 생각해내곤했다. 여전히 멋있는 남자로 말이다.

세월이 흐른 후 유튜브에서 동아방송기술대학의 실용음악과 친구들이 연주하는 것을 보게 되었다. 내가 꿈꾸던 모습을 그들이 연출하고 있었다. 특히 베이스를 치던 친구의 그 흥은 지금도 내가 그 영상을 찾아보게 만든다.

최원석 회장과 일면식도 없지만, 나는 어려서부터 동아건설을 삼촌덕에 알게 되었고, 뉴스에서 그를 보았고, 그의 사생활로 말미암아 어떤 젊은이들은 꿈을 펼치고 있다는 이 모든 과정이 알수 없는 도미노같고, 분명 연쇄된 사건임에도 그 사건의 주체자들은 서로 알지 못하며 직접적인 영향권 밖에 있는 것 같지만 사실은 영향이 있었기에 가능했던 일들이 아닌가 싶다.

오늘 우연히 말기암에 걸려 인생의 마지막 순간에 있는 그의 인터뷰를 보게 되었다. 그는 그의 인생을 어떻게 생각하고 있을까... 인터뷰에서 모든걸 이야기 하지 않았을테지만, 그는 역시나 멋진 셔츠를 입고, 멋진 남자의 모습이었다. 나는 말기암 환자도 멋있을 수 있다는 걸 처음 알게 되었다. 그가 비록 모든 걸 이야기 하지 않았을 것이고 하고 싶은말도 참고 많은 것을 되새기며 인내했음도 알지만 무엇보다도 그의 눈이 많은것을 이야기 해주고 있었다. 말은 참았지만 눈은 그러지 못하셨던것 같다.

그는 곧 아버지를 만나게 될 것이라 했다. 그는 그의 아버지를 좋아했고 의지했던것 같다. 아버지와 찍은 사진을 걸어두고 아버지를 기억하며 이야기하는 그는, 죽음앞에서 "아버지를 다시 만난다"라는 기대를 하고 있었다. 얼마나 보고 싶었을까... 얼마나 같이 이야기 하고 싶었을까... 얼마나 안겨서 울고 싶었을까... 사람들이 그에게 말도 안되는 돌을 던질때 그는 아버지를 생각했을것이다... 부인도, 자식도, 친구도 그 누구도 그를 용납하려 하지 않을때 그는 아버지를 생각했을 것이다. 아버지가 계셨더라면... 아버지가 계셨더라면...

내가 인터뷰어였다면 나는 분명 다른 질문들을 했을것이다. 지금도 여전히 안타깝다.

많은 생각을 하게 한다. 그가 곧 세상을 떠나면 세상은 다시 그의 무덤에 침을 뱉어댈것 같아 더욱 안타깝다. 이렇듯 세상은 옳지 않은 것이다. 세상은 정의롭지 않고 세상은 정확히 모르고, 세상은 누구든 난도질 할 준비가 되어있다. 나는 그가 진심으로 아버지와 함께 그 품안에서 위로받고, 수고했다 아들아 고생많았지... 라고 위로받길 원한다.

복음은 절대로 중요하다. 긴 아픔의 삶이후에 우리가 만날 그 위로를 위해서라도 복음은 반드시 살아서 만나야할 삶의 필수이자 목적이다. 복음없이 끝나는 삶의 뒤에 위로가 있으리라는 보장은 없다. 내가 하나님의 모든 것을 알 수 있는 사람이 아니기에 내가 알고 있는 한도내에서만 보자면, 복음은 유일한 삶의 끝에서 만날 진정한 위로이다.

최회장님께는 아버지가 계시기에 그는 죽음뒤에 삶을 기대하는 것이다. 막연하고, 비과학적이며, 누구도 증명하지 못했지만, 그는 곧 그가 아버지를 만날것을 믿고 있다. 아니 믿는다는 그 확신을 붙들지 않으면 안되기 때문에라도 그는 그의 기대를 투영하여 온 마음으로 그것을 그의 의식가운데 사실화하고 있는 것이다.

그가 예수님의 복음을 듣고, 십자가에서 예수님을 만난 강도의 고백과 같은 일로서라도 낙원에 가서 하나님 아버지의 위로를 받을 수 있기를 기도한다.

A SAFE is a form of convertible security. A SAFE isn’t debt; it’s a promise to issue future equity once certain terms are met.

SAFEs are a simpler alternative to convertible notes for early-stage startups looking to structure investments without interest rates, redemption rights, or maturity dates.

And to simplify things further, we’re sharing our pre-Money and post-Money Open Source VC SAFE templates!

What is a SAFE?

A Simple Agreement for Future Equity (SAFE) is a flexible agreement between an investor and a startup where in exchange for upfront money, the investor gains a contractual right to convert that amount into shares in the future when a pre-agreed trigger event occurs.

Early-stage startups use SAFEs to acquire money quickly and skip the typically time-consuming process of determining the valuation and carrying out comprehensive due diligence.

What is a trigger event?

A trigger event can include:

A priced equity financing round

An exit event, such as an IPO or acquisition.

Following a trigger event, the investment amount will convert into shares in the startup. In the case of a financing round, the SAFE will convert into the class of shares being issued in the round (e.g. Seed Preference Shares), and in an exit event, the SAFE will convert into ordinary shares.

The number of shares the investor receives depends on the initial cash payment amount, and the share price of the priced equity round or exit event. A startup may also agree to include a discount rate or valuation cap, which would apply to the relevant trigger event. This generally means that the investor receives their shares at a discounted price to the trigger event (in exchange for assuming additional uncertainty and risk in entering into the SAFE).

There may be scenarios where triggers aren’t activated, and the SAFE doesn't convert. For example, if your startup makes enough money that you never need to raise capital again, and you don’t get acquired by another company, then there may never be a trigger event for the SAFE conversion. Conversely, if your startup becomes, or is likely to become, insolvent, then SAFE investors are usually entitled to be reimbursed their investment amount.

SAFE terms

SAFEs contain a few primary terms that determine how they convert to company shares:

Valuation cap

A valuation cap is an agreed maximum value of your startup, which applies when a SAFE converts. When a trigger event occurs, the investor’s subscription amount will convert into equity relative to the valuation cap, even if your startup's valuation is higher than the cap.

When issuing a SAFE, the main thing to consider in terms of the valuation cap is the proximity to your startup’s next raise. If your startup is looking to raise in 6 months to 1 year’s time, the valuation cap will be relatively close to the value of your startup at the date of the SAFE investment. The valuation cap will likely be higher if the next raise is 1+ years away.

Discount

Startups may also include a discount rate in the SAFE. The discount rate applies to the price per share in the relevant trigger event. The investor’s subscription amount will convert at the trigger event’s price, less the discount rate. Discount rates are agreed and fixed in the SAFE – usually at 20% or less.

Most Favoured Nation

If your startup issues numerous rounds of SAFEs, a most favoured nation clause (MFN) causes any more favourable terms included in subsequent SAFEs (e.g. valuation cap, discount rate etc.) to automatically apply to any investors’ SAFE which includes an MFN. The MFN falls away once a SAFE has converted.

Valuation cap and discount scenarios

Valuation caps and discounts are commonly used in three different ways:

Valuation cap, no discount

In this scenario, the investor can convert their SAFE into shares based on the valuation cap. The valuation cap is the maximum possible valuation of a startup, even when the actual value of the startup in subsequent raises or an exit event is higher than the value specified in the valuation cap.

Discount, no valuation Cap

In this scenario, the investor’s SAFE converts into shares during a priced equity financing round or an exit event, at a discount to the relevant price per share in the respective trigger event.

In this scenario, Sarah is issued 22,222 shares (rather than 20,000 at $2.50 per share).

Valuation cap and a discount

Startups often include both a valuation cap and a discount rate in SAFEs. The SAFE works by applying the process (e.g. the discount rate, or valuation cap), which results in the investor receiving the greatest number of shares.

In this scenario, Sarah is issued 20,000 shares (rather than 13,888 shares under the discount).

Pro rata rights

Pro rata rights allow investors to invest extra funds to maintain their percentage of ownership during future equity financings. These rights are generally only granted to investors after the SAFE has converted into preferred shares of the company during an equity financing round. In some circumstances, startups will grant special pro rata rights to investors while they hold a SAFE.

An investor with pro rata rights isn’t required to invest anything into your next round, and founders should assume they have to earn investors’ pro rata investments in subsequent rounds. It’s also worth discussing with investors whether they hold reserves for each of their investments to take their pro rata.

Pro rata rights can be calculated in three different ways:

Percentage basis: Investors have the right to maintain their ownership percentage by continuing to invest more capital in subsequent rounds. This is the most common scenario.

Dollar-for-dollar basis: Investors have the right to invest an equal amount or lesser than what they invested before. This scenario is much less common.

Fixed-sum basis: Investors maintain the right to continuously invest an amount as agreed upon that is decoupled from the investment amount. This approach is not widely used.

Pre-money and post-money

A pre-money SAFE does not include the current SAFE in the company capitalisation (or any other SAFEs or convertible instruments). The company capitalisation is calculated before the SAFE converts, making it difficult to precisely calculate how much ownership the founder, team and investors will have when the SAFE converts.

On the other hand, post-money SAFEs include the current SAFE (as well as any other SAFEs or convertible instruments) in a company’s capitalisation, providing the company’s fully diluted capitalisation. Post-money SAFEs allow you to calculate specific ownership stakes and how much dilution has occurred with each SAFE.

Advantages of a SAFEs

Easy to create and implement As there is no need to agree on a pre-money valuation, SAFEs are quick and easy to negotiate. Founders can close with an investor as soon as both parties are ready to sign (and the investor is ready to transfer the funds), rather than coordinating a single close with multiple investors simultaneously.

No interest SAFEs don’t accrue interest, and founders can avoid the complexity of converting interest into equity.

No debt SAFEs are an equity, not a debt, and therefore don’t create the threat of insolvency for a startup.

No maturity or end date SAFEs can be held in perpetuity. There is no fixed date for when the startup must repay the SAFE, taking the pressure off founders and their timeline for a trigger event (e.g. a priced equity financing round).

Disadvantages of SAFEs

Dilution implications Founders can fall into the trap of not doing the basic dilution calculations associated with their ownership stake when the SAFE converts into equity. This results in founders owning less of their startup’s equity than they thought they did when an equity round is eventually priced.

Ignoring the signals Founders who cannot find a lead investor to price the round on the valuation and the terms they’re after, and instead choose to use a SAFE, may be ignoring the implicit message of the predicament they’re in.

This article does not constitute legal advice, and the SAFE document is only a template. You should always seek legal advice if you’re considering using this template.

Every startup begins with an ambitious founder and a great idea. But from there, they need money to build and grow. The good news is that many investors are looking to give capital to the right startup through various financing options – and one of those options is a convertible note.

To get you started, here’s are our Open Source VC convertible note templates (we've prepared pre-money and post-money versions), plus a quick overview of the terms you should know.

We’ve purpose-built the Open Source VC convertible notes for seed and early-stage companies, meaning they have reasonably basic and straightforward terms and a balanced approach between the interests of the startup and noteholders. Later-stage companies will likely use more complex, bespoke, convertible note documents.

It’s important to note that each Open Source VC convertible note is only a template. Founders should only use it them as a starting point and then update and personalise the document (with the help of a lawyer) to ensure it meets their specific requirements and circumstances.

What is a convertible note?

A convertible note is a hybrid security that converts into equity upon a predetermined trigger event. Trigger events typically include:

A qualifying equity financing round (e.g. company raises their Series A round from a credible external investor)

At an exit event (e.g. IPO, trade sale)

On the maturity date of the convertible note

Using a convertible note delays the need to determine the startup’s valuation until the startup carries out an equity financing round. This can be helpful for seed-stage startups with limited data points on traction, product and revenue or when there is no clear lead investor for the round.

We also see convertible notes used for internal bridging rounds, where the goal is to use the capital to achieve a milestone that will make the startup more attractive when it goes to raise a larger external round.

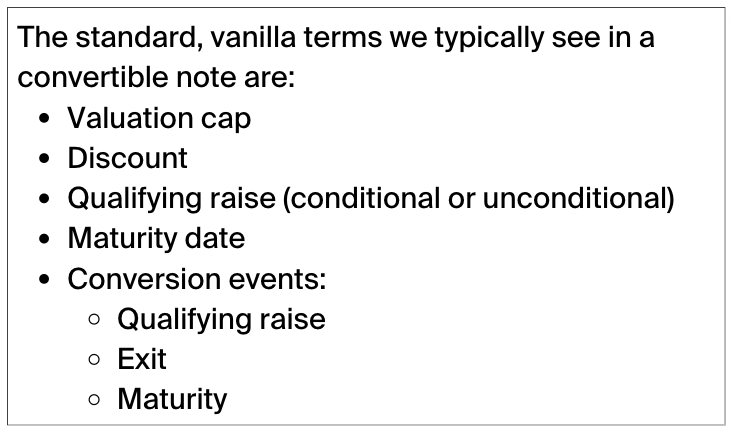

Convertible Note Terms

🍦Stick to the vanilla terms

Conversion - discount

A conversion discount is a mechanism to reward the noteholders for their investment risk by granting them the right to convert the loan amount at a discount to the purchase price paid by the investors in the equity financing round.

Discounts typically range from 10% to 35%, the most common being 20%.

The discount rate isn’t always static – it can increase. For instance, if your startup raises a qualifying round in 1 year, the investor gets a 20% discount. If the timeline to a qualifying round is beyond a year, it may go up to 30%.

Conversion - valuation cap

A conversion valuation cap is another mechanism to reward noteholders for their investment risk. A cap is a ceiling on the startup's value, determining the convertible note’s conversion price. Similar to a discount, it permits the noteholder to convert their loan at a lower price than the purchase price paid by investors in the equity financing round.

The interests of founders and investors are misaligned if the convertible note is uncapped (we wouldn’t consider this a vanilla term). Founders want the valuation to be as high as possible, while investors want the opposite, reducing their incentive to help a startup get to a higher valuation due to their introductions and operational support.

Conversion - discount and valuation cap

Convertible notes can include both a discount and valuation cap. Including a discount and valuation cap allows the noteholder to convert their loan into shares in the startup based on the mechanism that yields the lowest conversion price (and, consequently, the most shares). This is the conversion method included in our Open Source VC convertible note.

For example:

Sarah’s convertible note converts by dividing the loan amount ($500,000) by the valuation cap conversion price of $0.50. Sarah receives 1,000,000 Series A preference shares (375,000 shares more than the discount conversion price and 500,000 shares more than a Series A investor would receive for a $500,000 investment).

Interest rate

As a convertible note is a type of loan, the startup is sometimes required to pay interest (either simple or compound interest) on the loan amount. Interest isn’t always included in seed and early investments, but it’s commonly used in later-stage investments.

Unlike a typical loan where you pay interest periodically, it accrues until the conversion event. The total amount of interest is added to the loan amount (called the “outstanding amount”) and converted into additional shares when the convertible notes convert. We’ve included standard simple interest in our Open Source VC convertible note.

For example:

Qualifying financing

When a startup carries out a priced equity financing round (also called a “qualifying financing”), the convertible notes will automatically convert into the class of shares issued in the round.

For example, if the qualifying financing is a Series A round, the convertible notes will convert into Series A Preference Shares. The outstanding amount will convert into shares based on the conversion mechanics explained above – either the lower of the discount rate or valuation cap.

As a qualifying financing automatically converts the convertible notes to shares, sometimes founders and noteholders will want to ensure the value of the raise in the qualifying financing is material to the startup. To this end, a founder and noteholder may agree to make the qualifying financing conditional, meaning that the startup must raise a minimum amount of money at a minimum valuation (as opposed to unconditional, for which any qualifying financing is sufficient).

Qualifying financings are frequently used by later-stage companies concerning larger investments. However, as our Open Source VC convertible note is aimed at seed and early-stage startups, and to ensure simplicity, we’ve included unconditional qualifying financing.

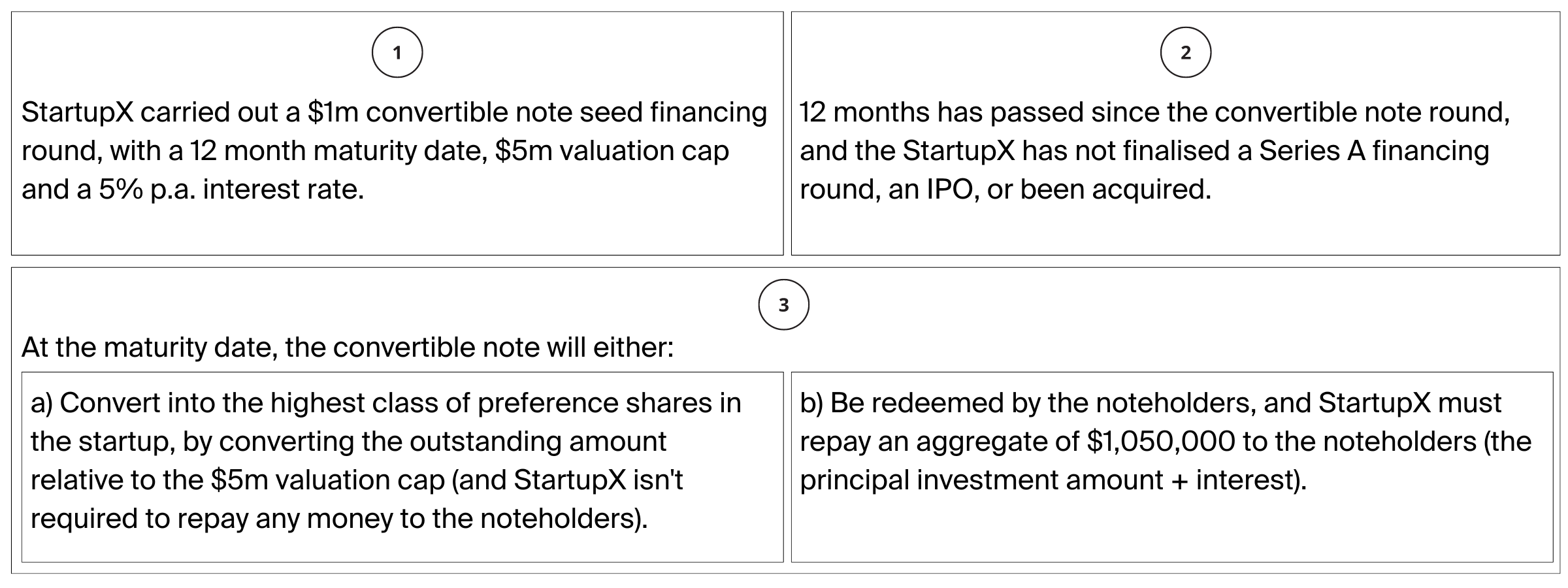

Maturity date

A convertible note will have a fixed maturity date, meaning that if a startup hasn’t already carried out a qualified financing or exit event, the convertible notes either converts into equity or the outstanding amount is repaid to the noteholders (also called “redemption”). Typically, the maturity date ranges from 12 to 24 months from the closing date of the convertible note.

If the convertible note converts at the maturity date, it will generally convert per the valuation cap method described above into the startup’s highest ranking class of preference shares at the time.

Alternatively, if the convertible notes are redeemed, the startup must cancel the convertible notes and repay the outstanding amount to the noteholders. Redemption can be problematic for startups as it may cause them to become insolvent in circumstances where a startup doesn’t have sufficient cash available to pay a noteholder its outstanding amount.

For example:

Given these risks, we’ve drafted our Open Source VC convertible note so that the convertible notes automatically convert into equity on the maturity date.

Exit event

When drafting the convertible note, founders should also address what happens if there is an exit event (which includes an acquisition of the startup or an IPO) before the maturity date. There are three different ways to approach this:

Repayment of the loan amount plus interest: the noteholders receive their investment amount plus any interest, but nothing else. The convertible notes don’t convert into equity or participate in the IPO or acquisition proceeds. In most circumstances, this is the most founder-friendly, but it’s less appealing for sophisticated investors as the return on their high-risk investment is only the interest of the loan. However, it does provide certainty to noteholders that they will at least receive their loan amount plus interest.

Conversion right: this provision permits the noteholder to convert the convertible notes into equity (generally using the same discount which is applied to the effective price per share in the exit event and valuation cap mechanisms above). Sophisticated investors prefer this approach as they can share in any upside if the startup is acquired.

Premium: this approach enables founders and investors to meet in the middle by including a provision that grants the noteholder the right to get their money back with interest, plus a premium. The premium is typically drafted as a multiple of the principal amount of the loan.

In an exit event, a noteholder is commonly granted the discretion to choose either the repayment of the loan amount plus interest or the conversion right. A premium is less common. Later stage companies usually have different considerations for the treatment of convertible notes on an exit event. They generally require conversion in circumstances of an IPO or scrip for scrip company sale (where shares of the company are swapped for shares of the company that is acquiring it).

Advantages of a convertible note

Speed and simplicity Convertible note financing can be faster and simpler than equity financing rounds. As convertible notes are classed as a hybrid security, there is no need to issue ordinary shares or create additional classes of preference shares. This removes the need to determine a company valuation, share option prices, and the related tax implications.

Maintain control Convertible noteholders are rarely granted control rights (e.g. a board seat or veto rights).

Disadvantages of a convertible note

Loan → Insolvency Convertible notes are a hybrid security that may require the investment amount to be paid back. If a startup fails to raise an equity financing round before the maturity date or to carry out an exit event, it may not have the funds to repay the outstanding amount. If the startup defaults on a convertible note, it can be pushed into insolvency.

Incentive to raise a qualifying round before maturity date If a startup has reached the breakeven point and doesn’t need to raise money before the maturity date, depending on how the maturity term is written, it may be a penalty to the startup. To avoid an adverse outcome, the startup may be incentivised to raise a qualifying round to set the conversion price.

Disclaimer: This article and the Open Source VC convertible note do not constitute legal advice. You should always seek professional legal advice if you’re considering using this template.

A little extra cash in the pocket never goes astray when you’re in the early stages of building your business. The process can be lengthy and tedious when it comes to Government Grants, but if your application is successful, it can give your startup a real leg up.

If you search the Government’s Grants and Programs finder, you’ll see that there are hundreds of opportunities opening and closing daily. So if you want to take advantage of these opportunities, you need to be aware of what’s on offer.

We’ve rounded up a list of the grants most relevant to early-stage startups.

National

Export Market Development Grants

Austrade’s Export Market Development Grants (EDMG) program helps Australian businesses grow their exports in international markets. Grants are categorised into 3 tiers, with each tier offering a different level of support:

Ready to export

Exporting and expanding

Exporting, expanding and strategic shift

Criteria

Your startup is eligible to apply if:

Your turnover for the financial year before the financial year in which the application is made is less than $20m

You have an ABN

You’re an Australian person as per the EDMG Rules 2021

What you can get

Cash reimbursements of 50%, up to $150,000 to claim on expenses related to:

Growth Grants help you improve a specific business area that an experienced facilitator has recommended in a roadmap or plan as part of a Growth service from the Entrepreneurs’ Programme.

Before you can apply for a Growth Grant, you must have received a completed plan from one of the following services:

Growth Roadmap: provides an analysis of your business by an independent facilitator to help you develop a roadmap to increase your availability to trade in Australia and/or other markets.

High Growth Accelerator: provides access to an independent facilitator for up to 2 years to help you develop a growth plan to realise an Australian and/or overseas growth opportunity.

SMART Projects and Supply Chains: provides you with access to strategic or high-value projects that increase business capability, meet the specific needs of a market opportunity, or otherwise improve business performance and leadership capacity.

Criteria

You must apply within 1 year of receiving a completed plan from one of the above Growth services.

The project that you apply for funding for must:

Have at least $5,000 in total, eligible project costs

Not have started

Link to an area of the business as specified in your plan

Give you new abilities to trade in Australia and other countries

Engage services outside of your business

What you can get

Funding of between $2,500 (ex GST) and $20,000 (ex GST), covering up to 50% of eligible project costs.

Accelerating Commercialisation helps startups get a novel product, process or service to market. There are two parts to it:

Commercialisation Guidance – guidance and assistance to develop your product or service’s commercialisation potential.

Accelerating Commercialisation Grants – financial assistance to help commercialise your product or service.

Criteria

The two key eligibility requirements are:

You have a novel product or service that you wish to commercialise for trade in Australia and/or an overseas market.

You meet the turnover test; you have a combined annual turnover of less than $20 million for each of the previous 3 financial years.

What you can get

You can get up to 50% of eligible expenditure to support your commercialisation project. You’ll also receive ongoing support from your Facilitator throughout the life of your commercialisation project.

The refundable tax offset is your corporate tax rate plus an 18.5% premium. If you’re running at a loss, you may be entitled to a 43.5% tax offset, paid as a cash rebate.

If you’re looking to access the CSIRO’s research expertise and capabilities, CSIRO Kick-Start provides matched funding that will enable your business to:

Research a new idea with commercial potential

Develop a novel or improved product or process

Test a novel product or material

Criteria

Your startup is eligible if you:

Have an Australian company number and are registered for GST

Can demonstrate your ability to dollar-match the funding

Have an annual turnover of less than $1.5 million, in the current and each of the 2 previous financial years

Have been a registered company for less than 3 years

What you can get

You’ll receive dollar-matched funding between $10,000 and $50,000. This funding may be used to cover the costs of undertaking a project, including:

The goal of the MVP Ventures program is to support businesses to increase the commercialisation of innovative products and services in NSW. Examples of projects include:

Prototyping and piloting studies

Development of current products through the implementation of new technology that will enhance competitive capability.

Criteria

MVP grants are available to startups developing scalable technology solutions. To be eligible, your startup must:

Be based in NSW and demonstrate that core activities include research and development.

Have an aggregated turnover of less than $1m for each of the 3 financial years prior to the lodgement of your application

Have less than or equal to 20 full-time employees.

The Backing Female Founders Program assists QLD female founders at different stages of the entrepreneurial lifecycle. There are 3 initiatives you can apply for:

Female Founders Co-investment Fund available to female-founded businesses undertaking a new pre-seed or seed capital raise.

Accelerating Female Founders Program available to eligible organisations to develop and deliver new or existing business support programs for Queensland female founders with innovative businesses.

The Female Founders Advisory Board Program delivers skills and exposure to effectively engage with advisors and establish best practice governance to support business growth.

Criteria

To be eligible for the Female Founders Co-investment Fund, applicants must:

Be a Queensland-based business

Have an ABN and be registered for GST

Be 100% female-founded business

Have no more than 50 full-time equivalent employees

Not received investment through previous capital raises, grant funding or accelerators totalling more than $500,000

Not be a current or past recipient of the Ignite Ideas Fund

Have secured pre-seed or seed eligible investment from an approved eligible investor

What you can get

The Female Founders Co-investment Fund provides grants from $50,000 to $200,000 matched at a 3:1 ratio over a period of 12 months, for either a single investment or a raise round led by an eligible investment entity.

The Innovation Booster Grant is part of the WA Government’s New Industries Fund, which assists WA-based startups and small businesses to commercialise their innovative ideas or projects and expand to create jobs.

Criteria

Your startup is eligible if:

It is registered in Western Australia and will continue to be based there for the next 3 years

You’re developing an innovative project in WA

You’re willing to, and have the financial capacity to contribute at least 20% of the requested project funding costs

What you can get

Funding up to $20,000 vouchers for eligible expenditure categories including:

When Hugh Williams first moved to the US in 2004, he was one of the early engineers to join the search effort at Microsoft. 15 years later he’s held several high-profile roles including VP Engineering and Product roles at Google Maps, eBay, Tinder and Pivotal. Hugh has now returned to Australia with a mission to help high school teachers develop their confidence and competence in teaching computer science — read more here.

We chatted with Hugh about everything from improving alignment between the Engineering team and PMs, to creating the right-sized teams for impact.

Here are a few key highlights.

Successful companies always have big, hairy, audacious goals

Company goals must have six things:

Ambitious (but not impossible) — if everything goes right, the company could pull them off

Simple — a relentless focus on one single goal can make a real difference

Mission-driven — something employees get excited about, and are proud of

Customer-facing — the only currency that matters

Measurable — displayed at the top of each team’s dashboard are the goals the whole company has bought into

Aligned right across the org — there should never be a situation where an Engineering lead is talking to the Product team and discovering they have different goals

This ensures that teams are not just working hard, but working on the things that are the highest priority to the company.

The 60:30:10 ratio

For Engineering leaders, getting the right balance for how you should spend your engineering resources is the hardest problem to solve.

A simple solution is to avoid the conversation about whose priority is more important (Product vs Engineering) and just agree on the split of energy you’ll spend working on the following:

Things that are product-related

Things that come from the engineering team

Innovation, the crazy wonderful things that Product or Engineering can do to delight customers and users

From experience, the ratio for the split of energy should be the following 60:30:10:

60% — focused on doing things defined by the product team e.g. the roadmap in order of priority

30% — focused on engineering priorities, including architecture, improving platforms, quality initiatives, and so on

10% — spent on some “free chaos”. Allow your team to work on innovative projects which could contribute to the 60% (product) or the 30% (“the house”)

There are times when the balance should swing to other ratios. For example, if everything is going great in the Engineering team it may mean you can spend a bit more energy on product (i.e. make it 70:20:10).

The right-size for your teams

From experience, it’s 6–8 people. If it gets larger, the complexity of point-to-point communication slows it down. If it’s smaller, teams don’t have enough resources to change the world.

When you have a tech team of 400 it’s not about managing a team of 400, it’s about setting up small 6–8 person organisations that feel independent, have customer-centric goals (so the lines between the teams are right), and can run really really fast.

It’s about the people

At a high level, when interviewing engineers make sure you look out for four things:

Intellectual horsepower — did you come out of the interview and think “wow, I learnt heaps”?

Problem solver — can they write real code in real language to solve a real problem?

Action-oriented — is this a person who stops talking and starts doing?

Results-driven — is this person focused on getting things done that matter? (action-oriented without the drive for results can be really dangerous)

Above all, hire people with raw horsepower.

These people that can do anything if they’re given the opportunity and the coaching.

Creating a strong, sustainable culture

There’s no silver bullet, but some basic principles are:

Constantly monitor — there’s a lot of power in communication, and not just about what’s going wrong

Constantly celebrate — hold up examples of what great looks like

Constantly fix — quietly deal with things that aren’t great

When things go wrong, always ask yourself in hindsight “why didn’t somebody fix that?”, and “why didn’t somebody keep celebrating the things that were important?”.

The Richmond Tigers (Melbourne AFL team) have a pretty inspirational story about turning their culture around. Have a read of the book “Yellow and Black” — it’s not just a story of a sports team, but how to get your team culture working again.